Dubai’s Bankers and Traders Make a Comeback, Yet…

The lunch gatherings have returned to the prestigious Arts Club within Dubai’s financial center, and the area’s roads are becoming congested once more. Many bankers, traders, and executives who temporarily left the United Arab Emirates due to Iranian missile threats are now beginning to return to their offices.

Following the US and Iran’s announcement of a ceasefire in early April, Dubai seemed to be finding its footing again. However, on Monday evening, emergency alerts urging residents to seek shelter indoors lit up mobile phones across Dubai and surrounding emirates for the first time in weeks.

Read: US efforts to end Iran war stumble as ship seized near UAE

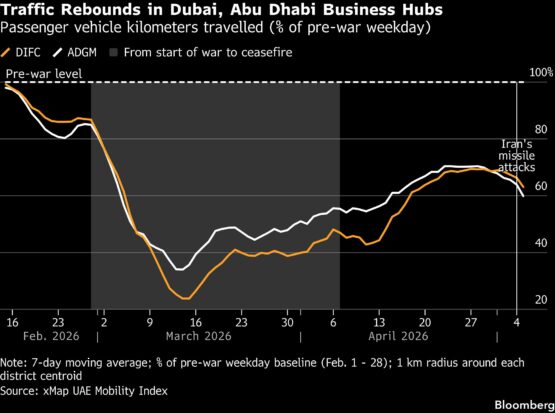

Schools, having recently reopened, reverted to online learning, and several financial firms adopted remote work protocols again. Traffic near the Dubai International Financial Centre, which had rebounded to about 70% of pre-war levels post-ceasefire, fell back towards 60% after Monday’s alerts, according to mobility analytics firm xMap.

The recent strikes targeting a port and offshore vessels near the UAE do not seem to have significantly shaken confidence.

Air defenses have been successful in intercepting nearly all projectiles aimed at the country, and many residents and businesses appear determined to maintain operations despite the instability.

Nonetheless, this brief disruption highlights the delicate balancing act facing the Gulf’s commercial hub as it strives to rebuild confidence while remaining aware of the potential for renewed conflict at any time.

“It serves as a reminder that despite a phase of stability, the broader situation continues to unfold and uncertainty lingers, even as everyone here is eager to return to normalcy,” stated Edwin Lawrence, CEO of Dubai-based advisory firm Nettlestone Capital Advisors.

Most finance professionals have remained in the city, helping to ensure business operations and essential services continue smoothly, while flexible and remote work arrangements have been initiated as necessary, according to the Dubai Media Office.

“As regional circumstances improved, employees have returned to standard in-person work arrangements.”

ADVERTISEMENT

CONTINUE READING BELOW

A Citigroup spokesperson stated on May 4 that “all employees are now welcome back to the office, and branches have resumed normal hours.” Standard Chartered Plc confirmed that its operations in the UAE and office attendance have returned to regular levels, declaring it’s “business as usual.” These policies are still in effect.

This resilience partly reflects the Middle East’s significance to financial institutions globally.

The region’s extensive capital reserves have been a vital source of funding throughout the years, and many executives pledged steadfast support to the Gulf during the height of the conflict.

Some firms are even continuing to invest. Brookfield Asset Management Ltd. is launching a property venture in Dubai, making a bold commitment to the city’s real estate market. “We understand the risks and benefits in the region better than others, and therefore are looking to invest,” said Jad Ellawn, managing partner and regional head at Brookfield Middle East.

Golden visas

These initiatives also reflect Dubai’s success in evolving into a less transient city. Although expatriates account for over 80% of the population, long-term “golden visas” have incentivized foreign workers to purchase homes and establish businesses.

Low taxes and safety continue to attract wealthy professionals and global firms, many of which are again hiring, “albeit at a slower pace,” noted Zahra Clark, head of Middle East and North Africa at Tiger Recruitment, which collaborates with financial companies for recruitment. “Approximately 20% of our pipeline has been put on hold,” she mentioned.

Even amidst unresolved conflict, hedge funds like Ken Griffin’s $67 billion Citadel are gearing up to begin operations in the emirate. Dubai has also relaxed some compliance requirements to assist firms in operating through the conflict.

In another indicator of confidence within the finance community, 258 companies set up regional offices in DIFC in March—a 59% increase from the previous year, according to a representative for the business hub. In total, 775 new firms were established in DIFC during the first quarter.

Greg Agius, CEO of Switzerland-based recruitment firm Agius & Partners, mentioned that numerous bankers and affluent individuals have been impressed with how the UAE has managed the crisis.

“Dubai offers a lot for families and business owners,” he remarked. “Switzerland may be lovely, but it’s slower-paced and bears higher taxes.”

ADVERTISEMENT:

CONTINUE READING BELOW

However, even as bankers return to their desks, the landscape for deals across the region is growing more uncertain. Many planned initial public offerings for the first half of the year are anticipated to face delays or cancellations, while mergers and acquisitions activity may decelerate as firms postpone investments, according to sources familiar with the situation.

Ripple in the economy

Beyond finance, the prolonged disruption has had a ripple effect throughout the broader economy.

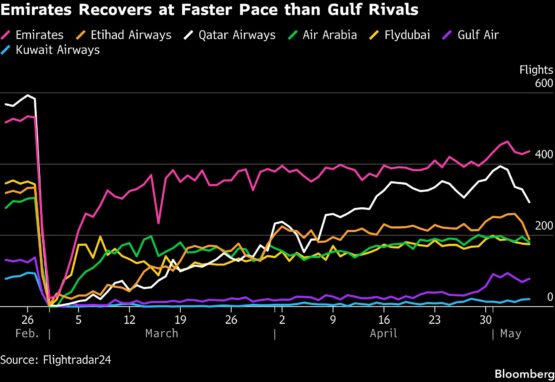

Emirates has bounced back faster than regional airlines but is still functioning at around 75% of pre-war capacity.

Hotel occupancy has plummeted to about 33% from over 80% prior to the conflict, as reported by CoStar Group.

Executives familiar with the circumstances expect activity to start increasing in a few months, just after the typically quiet summer period, with many Dubai hotels utilizing this time for renovations.

“Please keep in mind that we had years of nearly 85% occupancy in our hotels, at fantastic rates. We generated substantial profits,” stated Mohamed Alabbar, founder of Dubai’s Emaar Properties PJSC. “A temporary break of a few months is acceptable. We have time to maintain and refurbish our hotels.”

Residential rentals

On the rental front, home prices, which have steadily increased in recent years, have remained resilient in the face of war. Citywide, they have only dipped by just over 2% on average since the end of February, according to Prathyusha Gurrapu, head of research at property consultancy firm Cushman & Wakefield Core.

“Lease renewals are being signed at nearly the same rates as before, as many tenants prefer to avoid the expenses of moving,” she stated.

ADVERTISEMENT:

CONTINUE READING BELOW

Private schools, which experienced growth from Dubai’s expatriate influx, have had to navigate periods of online learning. Before Monday’s attacks, most students had returned to classrooms across the UAE, although attendance remained inconsistent.

Consumer spending behaviors are also beginning to shift.

Chipotle Mexican Grill Inc. observed a relatively swift recovery in Kuwait and Qatar, but a more gradual recovery in the UAE, as noted by CEO Scott Boatwright in an interview. The UAE attracts more tourists than the other two nations.

“Most local consumers are reverting to regular behaviors,” Boatwright commented. “I believe the principal challenge for the region presently is the decline in year-over-year tourism.”

In-store sales at the UAE’s main supermarket chains fell approximately 7% between March 30 and April 19 compared to the previous year, according to NielsenIQ. While online sales for these and other digital platforms saw a 15% rise, this growth was slower than the 34% increase rate prior to the conflict.

Despite the uncertainty, some executives remain optimistic. Emirates recorded a profit, albeit below earlier expectations.

The airline is “hopeful that this situation will resolve soon, facilitating a return to our February performance levels,” said President Tim Clark.

The head of the nation’s most recognized brand adopted a defiant stance last month.

“I don’t foresee any changes in how we operate the airline or this model,” Clark affirmed. “We’re not slowing down.”

© 2026 Bloomberg