Mexico’s Banks Distributed Millions of Unwanted Cards

Thirteen years after Uber entered the Mexican market, it faced an unforeseen challenge. Many citizens had smartphones ready to download the app, but a significant number were unwilling to pay via bank cards, either due to lack of access or preference against it.

Within a few years, the ride-hailing company introduced a cash payment option, which remains the preferred method for over half of its customers in the country.

This trend mirrors a wider issue: despite an increase in financial products available in Mexico, there remains an entrenched preference for cash. In many respects, the ease of digital services cannot compete with established cultural views on finance and a high rate of tax evasion, particularly outside metropolitan areas.

Read: Legal challenges and market conditions hinder Uber’s global expansion

On paper, Mexico is recognized as one of Latin America’s fastest-evolving fintech landscapes, hosting over 800 companies, a jump from under 200 a decade ago.

Electronic payment methods have surged at double-digit growth rates, fueled by millions in venture capital, with approximately eight out of ten Mexicans owning at least one financial product, according to government statistics.

The Uber app allows for cash payments in Mexico. Image: César Rodriguez/Bloomberg

However, more than half of Mexico’s debit cards remain unused, with almost 50% of credit cards sitting idle. This is largely due to banks and fintech firms pushing cards onto clients of their other services, a concern so widespread that last year, Mexico’s lower house approved a bill banning fees on these unsolicited items.

Cash continues to dominate everyday transactions, accounting for about 85% of small purchases based on government data.

Consider Roberto Negrete, a 33-year-old construction consultant from the State of Mexico. He manages nearly all his finances in cash, a habit passed down from his father.

When he receives his paycheck, Negrete visits Banamex, where he holds a checking account. Instead of depositing the funds, he exchanges his check for cash, which he then keeps in a safe at home. His bank account is used minimally, primarily for expenses like Netflix and Apple Music that require digital payment.

“I still prefer cash because it’s simpler and saving me from declaring my income, which would be tedious and confusing,” he states. “I dislike relying on a financial institution to handle my money. I prefer managing it myself.”

Read:

Progressing towards a cashless society

Uber now provides drivers with payment method options

Why Uber faces challenges in maintaining its tech identity

ADVERTISEMENT

CONTINUE READING BELOW

Negrete, like many Mexicans, uses the financial system when necessary but is hesitant to depend on it. This attitude stems from Mexico’s sizable informal economy and a lingering distrust in institutions formed after a banking crisis decades ago.

Roberto Negrete manages almost all his finances in cash. Image: Alejandra Rajal/Bloomberg

Approximately 54% of the workforce operates outside the formal economy, influencing how money is earned, spent, and saved. Cash offers privacy, while digital transactions create a paper trail that can make users susceptible to taxes.

Nonetheless, non-cash payments are gaining traction. By 2024, 19% of Mexicans preferred to make purchases over 500 pesos (around $29) using cards, a rise from roughly 12% six years earlier, per the central bank’s findings. Meanwhile, mobile or electronic payments became the favored option for 7.6% of consumers, increasing from just 0.3% in 2018.

A store in Tepic displays a sign stating, “Your Credit Cards Are Welcome.” Image: César Rodriguez/Bloomberg

“The primary reason people avoid digital payments is tax apprehension,” said Emilio Romano, the head of the Asociación de Bancos de México, in an interview. Thus, many consumers favor cash, with numerous merchants preferring it as well.

“Cash perpetuates a cycle that fuels everything from tax evasion to illegal activities,” Romano noted.

Read: PayInc intensifies efforts to transition South Africa to digital payments

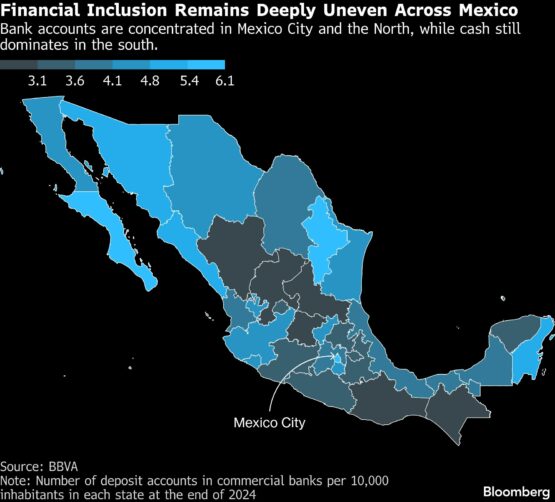

The aversion to banks intensifies with distance from urban centers. In Mexico City, a fintech hub, around half of all transactions are completed electronically, while cash still constitutes roughly 90% of payments in certain impoverished southern areas.

Mexico’s banking scenario lags behind that of the rest of Latin America. Although it is the second-largest economy in the region, just 63% of adults possess a bank account, per government data.

In contrast, over 90% of adults in Brazil utilize Pix, an instant-payment system launched in 2020 by the central bank, which quickly became the preferred method of payment in Brazil.

While Mexico has its own real-time payment systems, older, slower networks still operate concurrently, complicating financial transactions for businesses and institutions. Privately, many fintech executives claim that regulatory bodies have been sluggish in making changes that would promote adoption.

ADVERTISEMENT:

CONTINUE READING BELOW

Read: How Pix-enabled gangs exploit Brazil’s mobile payment boom

Nonetheless, firms like Nu Holdings Ltd, Banco Plata, Mercado Pago, and Klar have made progress after investing significantly, opening millions of accounts across Mexico. Others have struggled under competitive pressure: last year, Grupo Financiero Banorte sold its unprofitable digital bank to Klar.

In March, Femsa, one of Mexico’s leading retailers, laid off hundreds from its fintech branch amid tough market conditions.

A location in Tepic displays a sign stating, “No Card Payments Accepted.” Image: César Rodriguez/Bloomberg

Tamara Caballero, CEO of Banco Multiva SA, remarked that fierce competition in the finance sector has prompted larger, traditional banks in Mexico to adopt advanced technology, including artificial intelligence, to keep their existing clientele and draw in new customers hesitant to open bank accounts.

“Digitization will be a crucial catalyst for achieving financial inclusion,” she asserted. “It’s preferable to be part of the banking system and have access to financial products than to remain marginalized.”

Historical Anxieties

Distrust in Mexico’s banking system is deeply rooted in traumatic memories from the financial crises of the 1980s and 1990s, where banks shifted from state control to inexperienced private entities, leading to institutional failures and extensive taxpayer-funded bailouts.

Concealed skepticism towards banks persists to this day.

Government surveys indicate that only about 60% of Mexicans have faith that financial institutions will safeguard their money and data, while slightly more than half believe their complaints will be adequately addressed.

Moreover, some individuals remain wary of digital transactions. Grupo Elektra and Grupo Coppel operate retailers with in-store banking facilities, affording them an edge over fintechs among the underbanked due to their extensive locations nationwide.

“People trust the person, not the machine,” stated Rubén Coppel, financial services vice president at Grupo Coppel and chairman of BanCoppel, the firm’s banking division.

ADVERTISEMENT:

CONTINUE READING BELOW

Financial costs and complications further inhibit cash’s migration into the banking system. For instance, making a deposit at convenience stores typically incurs a fee of about 20 pesos ($1.15). Additionally, small businesses often face added costs and logistical challenges when accepting digital payments.

Mexico’s significant informal economy contributes to the lack of credit card usage. Image: César Rodriguez/Bloomberg

However, individuals outside the banking framework risk missing out on potential savings returns. While many traditional bank accounts in Mexico provide minimal interest, certain fintechs aim to attract customers with interest rates ranging from approximately 8% to 15%. Meanwhile, the value of cash that remains unbanked and uninvested diminishes as inflation rises.

“Once money resides in people’s accounts, resistance diminishes significantly,” remarked Carlos López-Moctezuma, CEO of BanCoppel. “The real challenge lies in the fact that cash is the starting point for millions of Mexicans, and converting it to digital forms incurs costs.”

Mobile-friendly solutions encounter hurdles when attempting to reach the unbanked. While 63% of fintech companies claim to serve underbanked individuals, only about a quarter report successfully reaching users who were completely outside the financial network previously, according to a survey from the Mexican Fintech Association.

The implications extend beyond individual consumers, as highlighted by Romano, the head of Mexico’s banking association.

Read:

Investec targets low-value payment sector

The shift towards decentralized finance

“Formalizing the economy fosters economic expansion,” he explained. “Entrepreneurs operating informally are unable to grow, as they must physically collect cash, can’t establish branches, and lack the ability to create a credit history.”

Industry leaders and policymakers are actively working to alter this scenario. Fintech firms strive to reduce user fees and streamline their products, while Romano noted that banks and the government are aiming to increase lending from approximately 38% to 45% of GDP by 2030.

In April, President Claudia Sheinbaum announced an initiative to lower transaction fees for card payments at gas stations, part of the government’s broader effort to diminish cash reliance.

Negrete, the construction consultant, acknowledges the changing landscape.

“One day I will have to go digital,” he shared. “Not out of preference, but out of necessity.”

© 2026 Bloomberg