Levi’s: Not the Next Nike – Part II

Two weeks ago, in Levi’s is not the next Nike, I discussed Nike’s gradual decline due to critical errors in developing its direct-to-consumer (DTC) strategy.

Now, I will examine how Levi Strauss & Co sets itself apart.

As a testament to Levi’s achievements, the company released an impressive quarterly report in April and even revised its guidance upward:

- Net revenues increased by 14% year on year, with organic revenue rising by 9% year on year, indicating growth in both volume and price across the board (a positive sign!);

- Diluted earnings per share (EPS) grew by 28%, while adjusted EPS increased by 11% year on year;

- Guidance for revenue growth was raised by 0.5%, and EPS guidance was lifted by an additional 2% year on year.

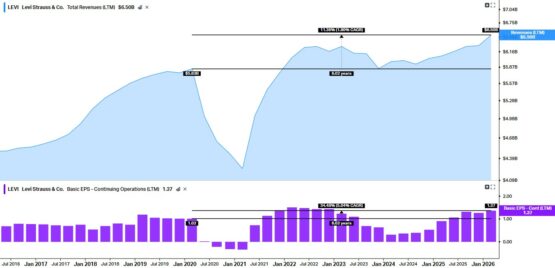

Levi’s revenue and EPS (12-month rolling to adjust for inherent seasonality in clothing)

Source: Koyfin

Despite the volatility caused by Covid taking time to stabilize, a review of Levi’s 12-month rolling sales clearly shows that the company is on a steady growth trajectory (refer to the chart above).

Since tracking began just prior to Covid, the company has achieved a revenue compound annual growth rate (CAGR) of 1.8% year on year and an EPS CAGR of 5% year on year, largely due to operational leverage.

Levi’s DTC sales have increased from 42% of total revenues in Q1/2020 (just before the pandemic began) to 52% in Q1/2026, with DTC growing by 16% year on year in the latest quarter.

ADVERTISEMENT

CONTINUE READING BELOW

What’s driving this growth?

In light of my previous article on Nike’s DTC-related downfall, how is Levi’s successfully expanding its DTC while also sustaining its other sales channels?

And how is it achieving this in the fiercely competitive denim market?

First, Levi’s has effectively expanded its product line (including branching out from bottoms to tops), which contrasts with Nike’s lack of innovation (see prior article).

Furthermore, Levi’s is connecting with cultural trends (evidenced by Beyoncé’s unendorsed song named after the brand!), while Nike has focused on data and applications.

Most importantly, the key distinction in their DTC strategies is that while Nike attempted to shift to a ‘DTC-only’ model, Levi’s adopted a ‘DTC-first, but not DTC-only’ approach.

Read:

Nike miscalculated by perceiving wholesalers and retailers as a “frictional cost” to eliminate; in doing so, it left an opening for competitors and provided them access to consumers.

Consequently, Nike lost consumer loyalty as a result.

ADVERTISEMENT:

CONTINUE READING BELOW

In contrast, under CEO Michelle Gass, Levi’s views its wholesalers as essential partners for market discovery.

While valuing its own Levi’s (and Beyond Yoga) stores, it has preserved strong relationships with high-end retailers and department stores.

This is clear from the Q1/2026 results, where DTC sales grew by 16% (as previously mentioned) and wholesale revenues increased by 12%.

A crucial note here: Wholesalers purchased more from Levi’s, not less.

This may seem too nuanced to matter, but these are very volume-sensitive business models. It is essential to nurture all avenues to market while ensuring product quality, innovation, and brand development are upheld.

Similarly, getting any one of these factors wrong can lead to severe, irreversible consequences (as shown in the chart below).

Levi Strauss versus Nike share price

ADVERTISEMENT:

CONTINUE READING BELOW

Source: Google Finance

In conclusion, I must acknowledge my misjudgment regarding Levi Strauss & Co.

Listen/read:

Is Levi Strauss the next Nike? [Aug 2021]

Last Levi’s factory standing [May 2016]

Levi’s is not the new Nike, thankfully. It seems to have learned from Nike’s catastrophic blunders in developing a crucial (yet risky) DTC-only sales channel.

Instead, Levi’s is paving its own path with a DTC and omni-channel approach that is more balanced – and with a market cap of only $8-9 billion compared to Nike’s $65 billion, it may have significant room to grow.

* Keith McLachlan is CEO of Element Investment Managers.

* McLachlan and the portfolios he manages may hold shares in Levi’s.